Get the pdf version: Investor Insights & Outlook June 2013

Get the pdf version: Investor Insights & Outlook June 2013

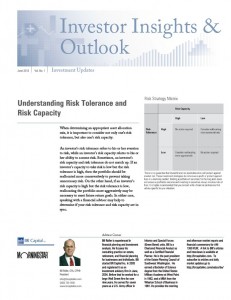

Understanding Risk Tolerance and Risk Capacity

When determining an appropriate asset allocation mix, it is important to consider not only one’s risk tolerance, but also one’s risk capacity.

An investor’s risk tolerance refers to his or her aversion to risk, while an investor’s risk capacity relates to his or her ability to assume risk. Sometimes, an investor’s risk capacity and risk tolerance do not match up. If an investor’s capacity to take risk is low but the risk tolerance is high, then the portfolio should be reallocated more conservatively to prevent taking unnecessary risk. On the other hand, if an investor’s risk capacity is high but the risk tolerance is low, reallocating the portfolio more aggressively may be necessary to meet future return goals. In either case, speaking with a financial advisor may help to determine if your risk tolerance and risk capacity are in sync.

What You Need to Know about Health Savings Accounts

Health Savings Accounts (HSAs) are growing in popularity, and more companies are offering them to their employees. Many people, however, are confused about what these plans are and when it is appropriate to take advantage of them.

What Is an HSA? Health Savings Accounts were created by a provision in the Medicare Prescription Drug Improvement and Modernization Act of 2003 and signed into law in December of that year. The purpose of creating the accounts was to provide a way for Americans to prepare for future medical costs and lower their health insurance premiums by switching to higher-deductible medical plans. Employers can establish plans for employees, and HSAs are also offered by banks, credit unions, insurance companies, and other approved companies.

In 2013, an individual can contribute up to $3,250 to an HSA, while families can contribute $6,450. People over 55 can also make a catch-up contribution of $1,000.

What Type of Tax Benefits Does an HSA Offer? Personal contributions offer participants an “above-the-line” deduction, which allows them to reduce their taxable income by the amount they contribute to their HSA. Participants aren't required to itemize their deductions to realize this benefit.

If your employer offers a “salary reduction” plan (also known as a “Section 125 plan” or “cafeteria plan”), you can make contributions to your HSA on a pre-tax basis. However, the “above-the-line” deduction is off limits for those who elect to contribute on a pre-tax basis.

If you are self employed, you cannot contribute to an HSA on a pre-tax basis. However, you can contribute with after-tax dollars and take the above-the-line deduction.

Who’s Eligible? In order to be eligible to contribute to an HSA you have to be covered by a high-deductible health insurance plan. "High-deductible" is defined as a deductible (where you pay the first dollars for medical service out of your own pocket) of $1,250 or higher for singles and $2,500 or higher for families.

In order to be eligible to contribute to an HSA, you cannot be 65 years of age or older. People 65 and older can maintain an HSA established prior to age 65, but they can no longer make contributions into it.

An HSA cannot be established for those eligible to be claimed as a dependent on another person's tax return. Also, if you are covered by another health insurance plan (such as a spouse's), you are not eligible for an HSA.

If you die and have money in an HSA, your spouse can use the account as if it were his or her own. If you are not married, the account can pass to a beneficiary but will no longer be considered an HSA and will be taxable to the beneficiary. If your estate is the beneficiary, the value of the HSA will be included on your final income tax return.

Making Withdrawals from Your HSA: Withdrawals made from your HSA are tax-free if used for qualified medical expenses. The same things you can deduct on Schedule A are considered medical expenses for HSAs. For more information on exactly what qualifies, see IRS Publication 502: Medical and Dental Expenses.

If you don't need to withdraw the funds from your HSA, you can let your contributions grow over time tax-free (similar to IRA accounts). HSA contributions grow on a tax-deferred basis. Moreover, unlike flexible spending accounts you may have used in the past, HSA contributions are not “use it or lose it.”

Monthly Market Commentary

As May saw spring slowly roll into summer, bond markets were sent into a tailspin by strong consumer confidence reports and real estate price data. Stocks managed to do better than bonds, but were still a little off as Germany and the rest of Europe decided to ease up on some of their austerity measures.

Employment: The U.S. economy added 175,000 jobs in May, just a little better than 149,000 in April, and the consensus forecast of 169,000. That's not far off the average for the previous 12 months, which is 179,000 jobs. Year-over-year average data has shown steady growth of around 1.9%–2.0% for almost two years, which is consistent with GDP growth of 2.1%–2.3%. Equity markets reacted positively to the employment numbers, but commodity and bond markets were not as thrilled. The jobs report was high enough to convince investors that the next recession wasn't around the corner, and just weak enough that Fed bond-buying programs are not likely to be eliminated in the very near future. The unemployment rate climbed to 7.6% in May from 7.5% in April.

Housing: Pending home sales showed a modest uptick in April, which should bode well for existing home sales in the months ahead. The Case-Shiller Home Price Index posted a 10.5% increase for April (calculated in year-over-year, 3-month average terms), indicating that the 6%–8% price appreciation seen in 2012 could be followed by a potential 8%–10% move in 2013. However, the Case-Shiller 20 is still about 28% below its all-time high, affordability remains near record-high levels, and not every geographic market is participating uniformly in the large increases. Also, low inventories and still-tight lending conditions are two major factors currently holding back the housing market.

Consumer Spending: The most important thing to remember when measuring this type of economic indicator is that month-to-month numbers fluctuate a lot and are not nearly as significant as long-term trends. Year-over-year data has been exceptionally stable and telling a story of slow and steady improvement. However, there is a sizable gap between income and spending. Spending itself remains stuck in the same 2% annual growth trajectory it has been on for more than two years. Meanwhile, income growth remains considerably below that level, which suggests that even if the consumer is optimistic, the fuel necessary for more spending is running a little low. Consumers in the top income quartile (who are big savers) really need to step it up spending-wise, and weather and gas prices need to cooperate to keep the U.S. economy from settling back a little in the second quarter and in the second half of 2013.

Trade: The U.S. trade deficit as a percentage of GDP has continued to shrink from 5.7% in 2005 to 2.9% in 2012 and 2.85% in the first quarter of 2013. The deficit has remained steady the last several years, even as the U.S. economy has entered a recovery (the trade deficit generally increases in a recovery and decreases in a recession). Continuing good news on the U.S. oil and gas front could improve the deficit even further. A smaller trade deficit points to a smaller need to borrow money from outside the U.S. and also generally means a stronger currency, which in turn helps control inflation.

Overall, Morningstar economists believe that 2013 may still turn out OK, with 2.0%–2.25% GDP growth, inflation well below 2%, and employment growth of about 1.8%. Real estate and consumer spending (especially on housing-related items) remain the bedrock to forecasts for the rest of the year. Government, business spending on structures and technology, and exports are likely to provide a headwind for most of 2013. The Affordable Care Act could be either a headwind or a tailwind. To get GDP growth much in excess of 2% now will require a few lucky breaks in weather, inflation, and Europe. All possible, but it's hard to take that to the bank. In fact, just a couple of bad breaks and the Fed's next move might be more loosening, not tightening.

The Importance of Saving for Women

Women face a different set of financial-planning challenges than men because they tend to live longer, earn less, and take more breaks from the work force. Women may also experience more difficulties if they are widowed or divorced. The good news is that women tend to save more. According to Vanguard’s “How America Saves 2012” report, women saved at rates about 5% to 10% higher than those of men across every income group. However, even though their savings rates were higher, women’s balances in savings accounts tended to be lower than those of men because women, on average, had lower incomes. This illustrates the extreme importance that saving (and starting to do so early) has for women. It’s not always easy, but managing debt, controlling expenses, and contributing to a retirement plan can make a world of a difference down the road.

©2013 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is intended solely for informational purposes; (2) is proprietary to Morningstar and/or the content providers; (3) is not warranted to be accurate, complete, or timely; and (4) does not constitute investment advice of any kind. Neither Morningstar nor the content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. "Morningstar" and the Morningstar logo are registered trademarks of Morningstar, Inc. Morningstar Market Commentary originally published by Robert Johnson, CFA, Director of Economic Analysis with Morningstar and has been modified for Morningstar Newsletter Builder.